Search Massachusetts Property Tax Records

Massachusetts property tax records are held by each of the state's 351 cities and towns, which means you search at the local level. This guide shows you how to find property assessments, tax bills, and parcel data across all 14 counties in Massachusetts, whether you search online or contact your local assessor's office directly.

Massachusetts Property Tax Records Overview

How Massachusetts Property Tax Records Work

Property tax in Massachusetts is managed at the municipal level. Each of the 351 cities and towns has its own Board of Assessors with independent authority to assess property. There is no single county assessor. This is different from many other states. When you search for Massachusetts property tax records, you go to the city or town where the property sits, not the county courthouse.

Under MGL c. 59, §38, all property must be assessed at 100% fair cash value, which means market value. Assessors are required to conduct full revaluations on a regular cycle, and the Department of Revenue's Division of Local Services certifies each municipality's assessment program. The DLS reviews assessments to make sure local boards are following state law. You can reach the Division of Local Services at (617) 626-2300 or by email at dls_alerts@dor.state.ma.us.

Your property tax bill is calculated with a simple formula. Divide the assessed value by 1,000, then multiply by the tax rate. The rate is set by each municipality annually after the DLS approves it. Residential and commercial properties can carry different rates in towns that adopt the split classification option. The DLS publishes all approved tax rates through its DLS Gateway data portal, where you can look up rates for any city or town going back decades.

Most communities in Massachusetts send quarterly tax bills. Due dates fall on August 1, November 1, February 1, and May 1. Some smaller communities still use semi-annual billing. If you miss a payment, interest accrues at 14% per annum under state law. Extended delinquency can lead to a tax taking by the municipality, and in serious cases, the Massachusetts Land Court handles tax lien foreclosure proceedings.

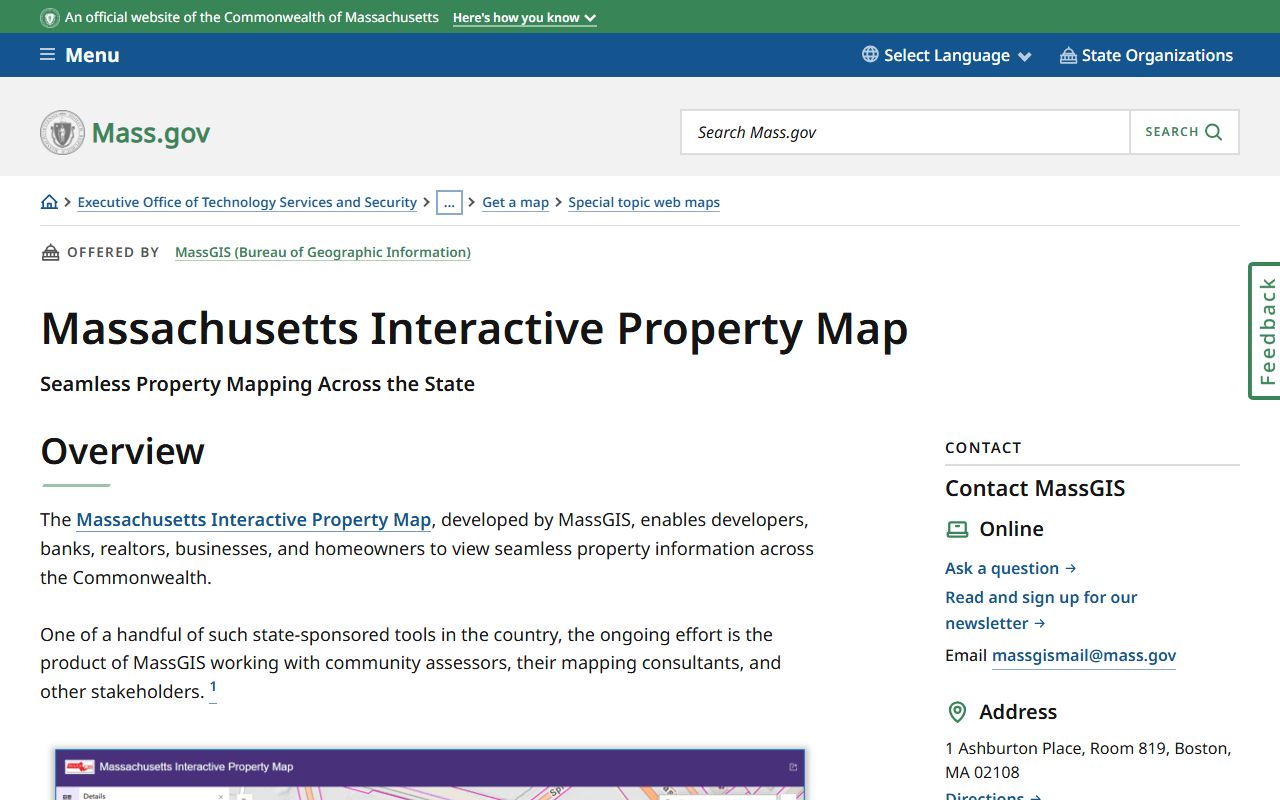

The screenshot below shows the Massachusetts Interactive Property Map, which is one of the best free tools for finding property tax records across all 351 communities. The map is run by MassGIS and lets you click on any parcel to see assessed values, owner information, and sale history.

Visit the Massachusetts Interactive Property Map on mass.gov

The Massachusetts Interactive Property Map covers all 351 cities and towns and is free to use with no account required. You can search by address, parcel ID, or owner name.

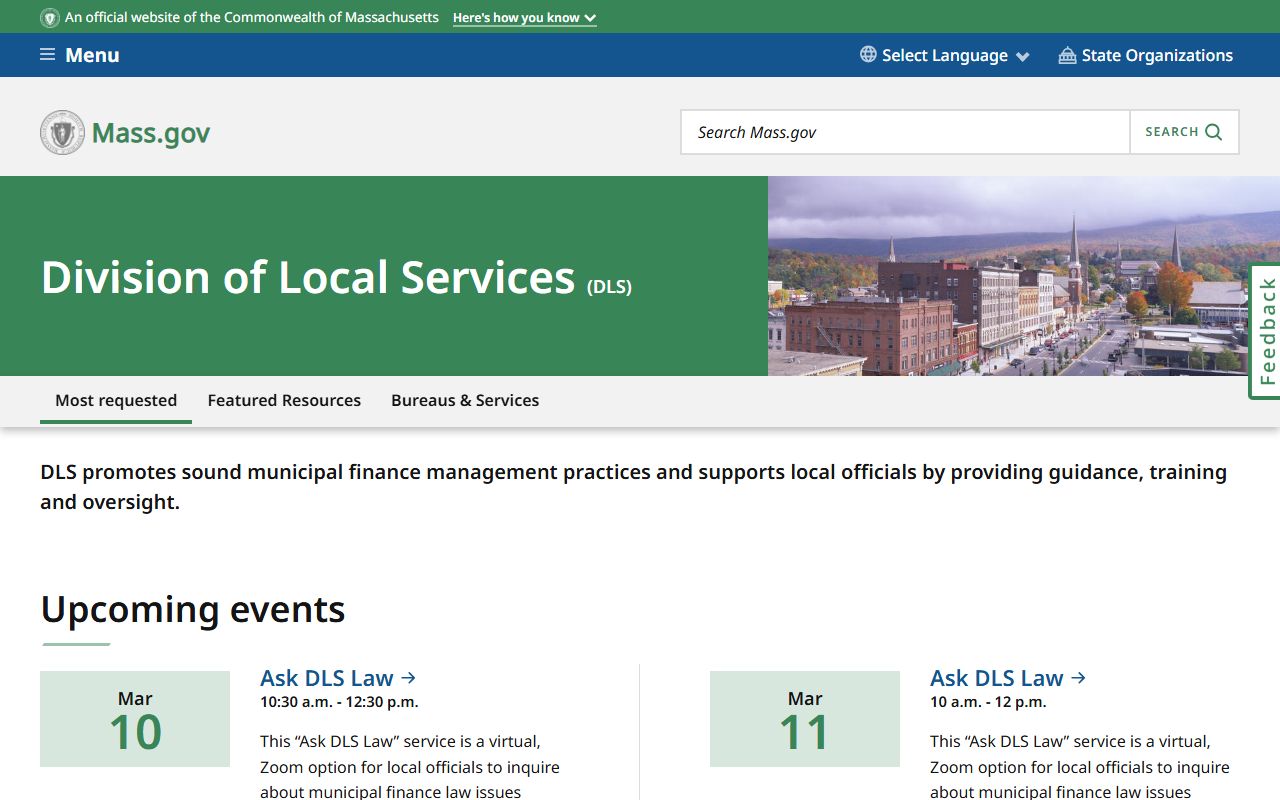

The DLS homepage shown below is the starting point for most property tax research at the state level. From there you can get to the Municipal Databank, the tax rate reports, and the local assessors directory.

Visit the Division of Local Services on mass.gov

The Division of Local Services approves tax rates, certifies assessments, and provides technical assistance to local boards of assessors throughout Massachusetts.

Note: The DLS Municipal Databank at the DLS data portal has historical tax rate data going back to the 1980s, which is useful if you need to research assessed values over many years.

Statewide Property Tax Search Tools

Massachusetts offers several free tools to search property tax records without contacting a local office. These tools pull data directly from municipal assessors and are updated regularly. Knowing which tool to use depends on what you need.

The Massachusetts Interactive Property Map is the most complete statewide option. Developed by MassGIS, it displays property boundaries for all 351 communities and shows assessed land value, building value, total assessed value, year built, living area square footage, property use code, last sale date and price, and owner name and mailing address. You can search by street address or parcel ID. The map also lets you export data to CSV and print customized maps. It is free and requires no login.

The Property Information Finder provides the same assessment data as the interactive map but in a text-only format. It is designed to meet 508 accessibility standards for users with screen readers. You search by street address and town. Results come back in a table format that works with assistive technologies.

For deed copies, MassLandRecords.com is the free official source for recorded documents. You can search by grantor, grantee, or address and download deed copies at no cost. Some third-party companies charge fees for this same free service, so go directly to MassLandRecords to avoid unnecessary charges.

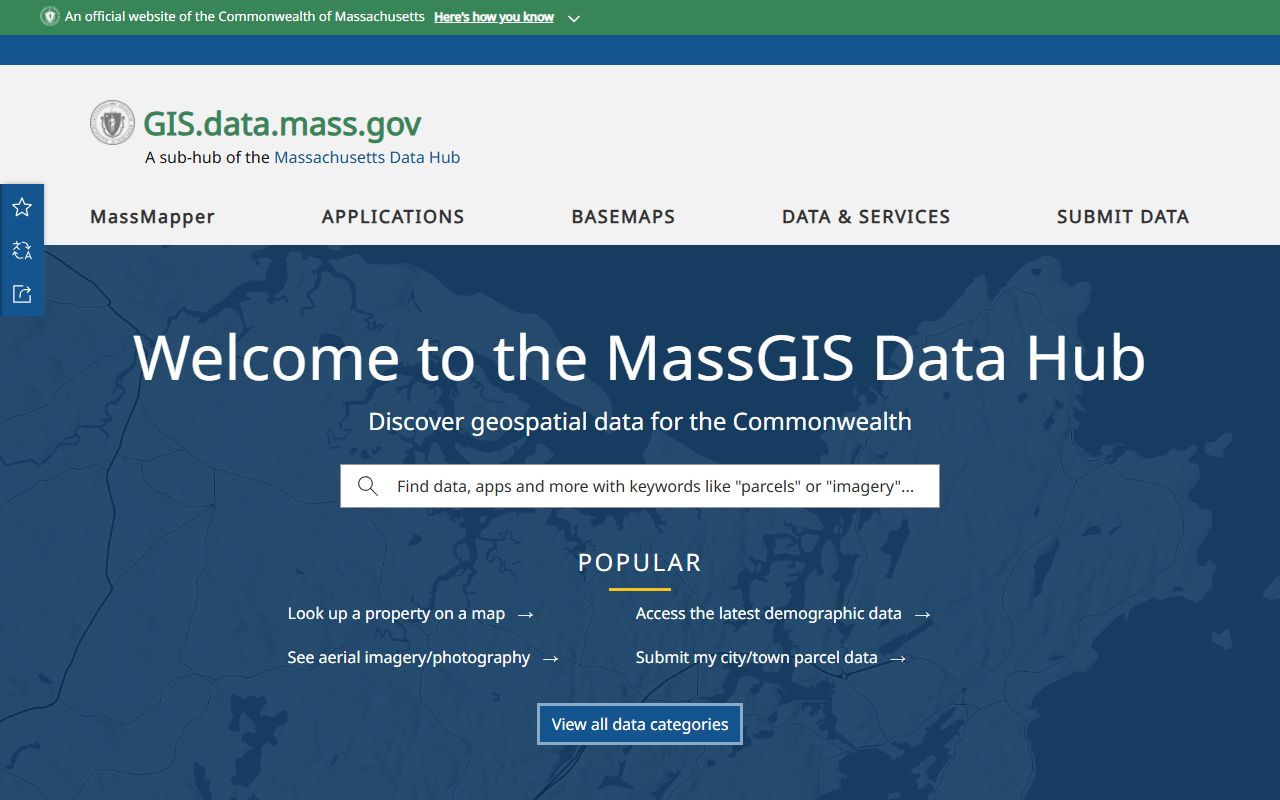

The MassGIS Data Hub shown below provides raw GIS data downloads for developers and researchers. You can get complete statewide parcel datasets in shapefile, geodatabase, GeoJSON, or KML format.

Visit the MassGIS Data Hub at gis.data.mass.gov

The MassGIS Data Hub lets you download standardized property tax parcel data for all 351 Massachusetts communities. The dataset includes parcel boundaries and assessment database fields, and it is updated quarterly.

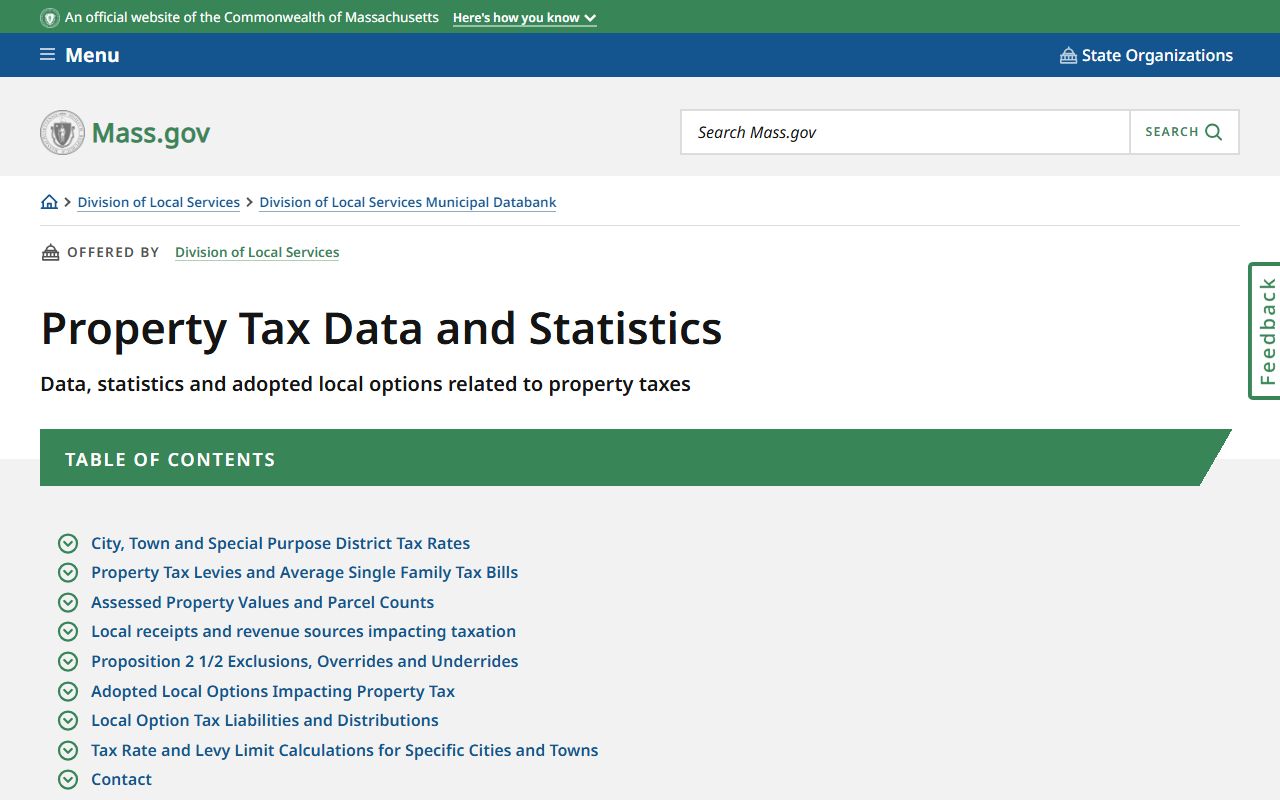

The property tax data and statistics page shown below lists reports compiled by the DLS, including average single-family tax bills, tax rates by classification, and Proposition 2½ override data for every city and town.

View property tax data and statistics on mass.gov

The DLS publishes annual property tax data reports covering assessed values, tax rates, and average bills for all Massachusetts municipalities. These reports are free to download and cover multiple fiscal years.

You can also find the local assessors directory on mass.gov, which lists contact information for every Board of Assessors in the state. This is the right place to start when you need to contact a specific city or town about a property tax bill or assessment question.

Note: For the most current assessment data, go directly to the local assessor's website for the city or town where the property is located. State tools update on a lag, and local databases are often more current.

Proposition 2½ and Massachusetts Property Taxes

Proposition 2½ is one of the most important laws shaping property taxes in Massachusetts. Voters passed it in 1980, and it is now codified at MGL c. 59, §21C. The law sets two key limits on how much cities and towns can raise through property taxes each year.

The first limit is a levy ceiling. A city or town's total property tax levy cannot exceed 2.5% of the total full cash value of all taxable property in the community. The second limit is an annual increase cap. Each year, the levy can only go up by 2.5% over the prior year's levy limit, plus the value of any new growth from new construction or development. The tax rate itself cannot exceed $25 per $1,000 of assessed valuation under this cap.

Communities can exceed these limits only with voter approval. A Proposition 2½ override allows a permanent increase in the levy limit, but it requires a majority vote at a local election. An exclusion is a temporary addition to the levy, typically used to fund a specific capital project like a school building, and it expires when the debt is paid off. Override and exclusion votes are tracked in the DLS Municipal Databank.

Note: Proposition 2½ affects the total levy that a city or town can raise, not the tax rate directly. Your individual tax bill can still go up even in a year with no override if your assessed value rises faster than the average.

Massachusetts Property Tax Exemptions

Massachusetts law provides a range of property tax exemptions under MGL c. 59, §5. These exemptions reduce or eliminate the property tax burden for qualifying individuals. Each exemption is identified by a clause number, and most require an annual application to your local Board of Assessors. The deadline is typically April 1 or three months after the actual tax bills are mailed, whichever comes later.

Veterans have several exemption options depending on disability status. Clause 22 gives a $400 exemption to veterans with a 10% or higher VA service-connected disability rating, Purple Heart recipients, and Gold Star parents. Clause 22A raises that to $750 for veterans who lost use of a hand, foot, or eye. Clause 22E provides $1,000 for veterans with a 100% VA disability rating. Clause 22D and Clause 22F offer full exemptions, with 22D covering surviving spouses of service members killed or missing in action and 22F covering paraplegic veterans and those with 100% service-connected blindness.

Senior citizens have options too. Clause 41C offers an exemption for seniors age 70 and older, or 65 and older in communities that adopt it by local vote. The amount typically ranges from $500 to $1,500 depending on the town. Clause 41A is a tax deferral rather than an exemption. It lets seniors with income under $20,000 delay paying their taxes until the property is sold or the owner passes away. Deferred amounts accrue interest at a rate not to exceed 8%. Blind persons qualify for a $500 exemption under Clause 37A.

A few communities also offer a residential exemption, which reduces the taxable value of a primary residence by a percentage of the average residential assessed value in that town. Boston, Cambridge, Somerville, Brookline, Malden, Waltham, and Everett are among the communities that use this option. You must own and occupy the property as your primary residence to qualify.

The Massachusetts property tax laws page shown below is a helpful reference that collects statutes, guides, and DLS bulletins related to exemptions and abatements in one place.

View Massachusetts property tax laws on mass.gov

The property tax laws page on mass.gov gathers key statutes, DLS guidance letters, and training materials for taxpayers and assessors. It is a good starting point when researching exemption eligibility.

The MGL c. 59 exemptions page shown below displays the full text of the exemption clauses. Reading the actual statute helps you understand exactly what documentation you need to provide when applying.

Read MGL c. 59, §5 on mass.gov

MGL c. 59, §5 lists all property tax exemption clauses in Massachusetts. The clauses cover veterans, seniors, blind persons, surviving spouses, and others. Read the specific clause you plan to apply under before visiting your assessor.

Senior Circuit Breaker Tax Credit

The Senior Circuit Breaker is a state income tax credit, not a property tax exemption. It is available to seniors age 65 and older whose property taxes are more than 10% of their annual income. The maximum credit for 2025 is $2,820. You claim it on your Massachusetts income tax return using Schedule CB.

To qualify in 2025, your income cannot exceed $75,000 if you are single, $94,000 if you file as head of household, or $112,000 if you are married filing jointly. The assessed value of your home cannot exceed $1,298,000. The credit applies to both homeowners and renters. Renters use 25% of the rent they paid as their property tax figure for the calculation. The full program details and eligibility requirements are on mass.gov.

The Senior Circuit Breaker page shown below explains how to calculate the credit amount and what documentation you need when filing. The page also links to Schedule CB and the instructions for completing it.

Visit the Senior Circuit Breaker Tax Credit page on mass.gov

The Senior Circuit Breaker gives eligible seniors a direct credit against their state income tax. The maximum credit of $2,820 for 2025 can offset a meaningful portion of an annual property tax bill for those who qualify.

Senior tax deferral is another option for those who do not want to sell or move but struggle with large tax bills. The deferral FAQ page shown below covers how the program works and what happens to the deferred balance over time.

Read the senior tax deferral FAQ on mass.gov

Tax deferral under Clause 41A lets eligible seniors postpone their property tax payments rather than pay them each year. The deferred amount becomes due when the property is sold or the estate is settled.

Note: The Circuit Breaker credit and the Clause 41A deferral are separate programs. You may be eligible for one but not the other. Check with your local assessor or a tax professional to see which option fits your situation.

Abatements and Property Tax Appeals

If you think your property is assessed too high, you have the right to file for an abatement. An abatement is a reduction in your assessed value. You file Form ABT with your local Board of Assessors. The deadline is April 1 of the fiscal year or three months after the actual (not preliminary) tax bills are mailed, whichever is later. Filing is free. You must continue to pay your taxes while the application is pending, or you lose your right to appeal further.

The grounds for an abatement include overvaluation of your property compared to market value, a disproportionate assessment relative to similar properties, misclassification between property types such as residential versus commercial, a mathematical error, or a denial of a statutory exemption. You will need to gather evidence to support your claim. Comparable sales data from nearby properties is the most common type of evidence. Some assessors will also consider an independent appraisal.

If the assessors deny your abatement or take no action within three months, you can appeal to the Appellate Tax Board. The ATB is a quasi-judicial state agency that hears property tax disputes. Under MGL c. 59, §59, you have three months from the assessors' decision to file your appeal with the ATB. The board is located at 100 Cambridge Street, Suite 200, Boston, MA 02114. You can reach them at (617) 727-3100 or by email at atb@atb.state.ma.us. Office hours are Monday through Friday, 8:45 AM to 5:00 PM.

ATB filing fees depend on the assessed value of your property. Properties assessed at $20,000 or less pay $10. The fee is $50 for assessed values between $20,000 and $100,000. For values between $100,000 and $999,999, the fee is $100. Properties assessed at $1 million or more pay 0.10% of the assessed value, up to a maximum of $5,000. The ATB offers two procedures. The Formal Procedure follows full rules of evidence and preserves your right to appeal to the Massachusetts Appeals Court. The Informal Procedure has relaxed rules but limits your right to appeal further. The ATB website explains both options in detail.

The ATB appeals guide shown below is a practical resource that walks taxpayers through the entire process from filing Form ABT through the ATB hearing.

Read the real estate tax appeals guide on mass.gov

The ATB appeals guide covers the abatement process, deadlines, evidence requirements, and what to expect at an ATB hearing. It is written for both taxpayers and assessors and is available at no cost on mass.gov.

The Appellate Tax Board homepage shown below has links to forms, filing instructions, and recent decisions. You can also find information about scheduled hearings and how to request a continuance.

Visit the Appellate Tax Board on mass.gov

The Appellate Tax Board hears property tax disputes from taxpayers across all 351 Massachusetts municipalities. Filing an appeal with the ATB is a formal legal process, so review the filing requirements carefully before you submit.

Note: You must file your abatement application on time to preserve your right to appeal to the ATB. Missing the April 1 deadline means you cannot challenge your assessment until the following fiscal year.

Property Tax Payment and Due Dates

Most Massachusetts cities and towns use quarterly billing. Bills go out in advance, and payments are due on August 1, November 1, February 1, and May 1. The August and November bills are preliminary bills based on the prior year's taxes. The February and May bills are the actual bills based on the current year's assessed value and tax rate. If the actual bill differs from the preliminary, the difference is spread across the last two payments.

A smaller number of communities still use semi-annual billing, where payments are due twice a year. Check with your local tax collector to confirm which schedule applies to your community. Some cities and towns also offer auto-debit payment options to avoid missed deadlines.

Late payments accrue interest at 14% per annum under Massachusetts law. If taxes go unpaid for an extended period, the city or town can begin a tax taking. A tax taking creates a tax title on the property. The municipality holds this tax title, and if it remains unpaid, the community can pursue foreclosure in the Massachusetts Land Court. Once foreclosure is complete, the owner loses the property. Recent federal court decisions, including Tyler v. Hennepin County in 2023, have affected how states must handle any excess equity when foreclosing on a tax title, and Massachusetts has been updating its procedures as a result.

Browse Massachusetts Property Tax Records by Location

Massachusetts property tax records are held at the city and town level. Select a county or city below to find local Board of Assessors contact information, search portals, and property tax resources for that area.

Massachusetts Property Tax Records by County

Each county links to a page with detailed information about the municipalities in that county, local assessor offices, and how to search property records in that area.

View All 14 Massachusetts Counties

Property Tax Records in Major Massachusetts Cities

Residents of these cities file property tax documents and request records through their city's Board of Assessors. Select a city below for local assessor contact info, search tools, and tax record access details.